Q2 Market Recap

Imagine you were given two pairs of special glasses that were designed to look backward in time rather than forward in space. The first pair can only see how the markets did; the second pair is designed to focus on the economy.

Each would give you a very different picture of how the second quarter went.

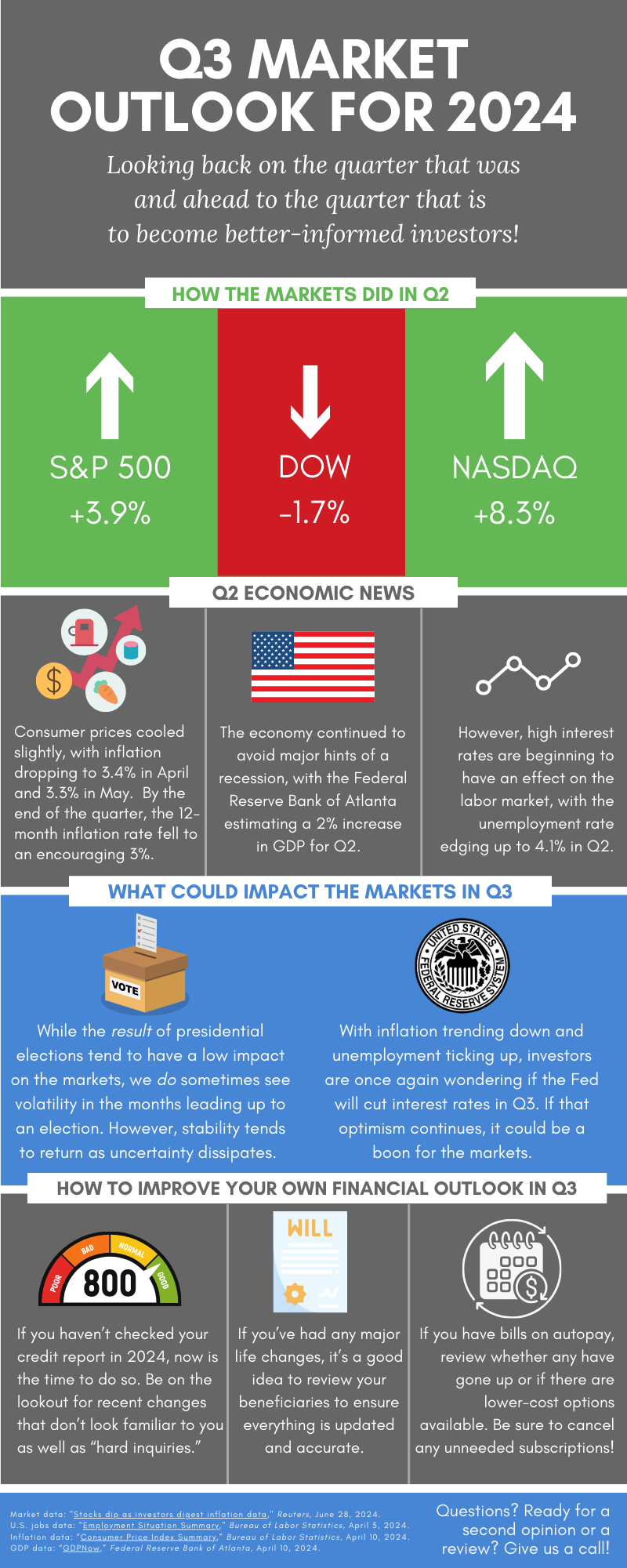

The first pair would show you that the markets had their best quarter since 2020. The Dow gained nearly 13%. The S&P 500 rose 14.9%. And the Nasdaq shot up an astonishing 21%!1

The second pair, the one that sees the overall economy, has a less rosy view. In fact, it would show you a picture of an economy in some distress. An economy where the annual inflation rate rose to 4.2% in May, the highest in three years.2 An economy where consumer confidence fell to historically low levels in April and May (although it did rebound slightly in June).3 An economy that may have only grown slightly in Q2 compared to its historical average.4

Both glasses are functioning properly. Both have the same maker. So why such different views? How can the markets be flying when the economy is grounded, and vice versa?

It’s not hard to understand why the economy had the quarter it did. Turmoil in the Middle East sent a shockwave through the oil and fertilizer markets, causing the goods and services that depend on those things to rise in price. (Think food, gas, electricity, transportation, and more.) By extension, a higher cost of living depresses consumer confidence. After all, it’s hard to feel confident about the future when more and more of your paycheck gets eaten up by simple necessities every month. And when consumer confidence drops, consumer spending drops…leading to slower economic growth overall.

The markets can be a bit harder to parse, but a closer look at what types of stocks performed well can provide the answers. Remember how we said the Nasdaq rose 21%, compared to 14.9% and 13% by the S&P and Dow? Well, the Nasdaq is primarily composed of technology companies. It’s those same companies that powered the S&P 500’s growth. A good example is semiconductor stocks, which surged 87.8% for the quarter.5

Tech companies have been the stock market’s main mover for years now due to the hope and hype around AI, and that story continued in Q2. What’s interesting, however, is that while the story remains the same, the characters inside it have changed. You see, just as the tech sector has been the single biggest propellant of the market, the sector itself has been largely driven by a handful of companies like Alphabet (Google), Amazon, NVIDIA, META (Facebook), Microsoft, Apple, and Tesla. These “Magnificent Seven”, as they are commonly known, have been at the forefront of the AI boom, and it’s their growth that has lifted the overall markets.

But that wasn’t the case in Q2. In fact, the Mag 7 fell during the quarter, and most have been essentially flat or even negative for the year overall.6 Instead of AI companies, investors paid more attention to AI infrastructure. (Again, semiconductors are a great example, as without them, we would lack the raw computing power needed to run AI.) In other words, it’s not the companies mining for gold, but the ones providing the picks and shovels that did well in Q2.

But none of this addresses the question we posed earlier. How can those two pairs of glasses show such diametrically different views?

The answer is a simple but critical truth: The markets and the economy are not the same.

The economy is how much our country produces and consumes. It’s the sum total of everything we make, buy, trade, and use. It’s the economy that drives our daily experiences.

The stock market, on the other hand, represents something far less tangible. It is the sum total of what we think, expect, and, yes, hope will happen in the future. It’s the market that drives our dreams and goals.

Politicians and pundits often like to use these two terms interchangeably, depending on which one makes them look better. Most common is when the markets are used as a stand-in for the economy. That’s because, while the markets are often hard to understand, they are easy to read: They go up or they go down.

As investors, though, it’s important that we remember that each is different and affected by different things. That’s because our feelings about the economy can sometimes color our opinions of the markets. This is largely due to something called status quo bias: The feeling that the current state of affairs will go on forever. When we feel frustrated or exuberant about the economy, it can impact how we invest, and not always in predictable ways.

For example, it’s easy to picture someone who, feeling negative about the economy, lacks confidence in the future and decides not to invest. But economic angst can also cause people to take more risk in the markets. In fact, there is some indication that is happening now. A recent survey found that 80% of Gen Z respondents — people born in the late 90s and early 2000s — often make “high-risk or speculative” investments because they feel financially left behind.7 And the Federal Reserve reported last year that American households now hold an all-time high of 45% of their total financial assets directly in stocks.8

That surpasses the previous record set during the dot-com bubble.

More stock market participation is generally a good thing, and it’s probably another reason why the markets performed well in Q2. But it can be a red flag when more and more people are taking on more and more risk due to their feelings about the economy.

On the other hand, market exuberance can sometimes make us forget the realities of the economy…realities that may eventually impact the stock market. Higher inflation can lead to higher interest rates. When both become “sticky,” it can prompt fears of a recession, which in turn can drag down the markets. (We experienced this in 2022.) Failing to remember this can also cause investors to start chasing ever higher returns, forgetting all about risk in the process.

The point, is to emphasize that there are two mistakes investors can make when it comes to the relationship between the markets and the economy. The first is to confuse one for the other, or to use one to drive our decisions regarding the other.

The second is to ignore one and focus solely on the other, forgetting that, while they are different, they do have a relationship…and there are times when both can converge.

Remembering this is all the more important after a great quarter in the markets. We cannot predict the future, of course, so it’s quite possible the economy will improve in Q3, and that the markets will continue progressing upward. But when the economy and the markets diverge this sharply, it’s worth asking ourselves whether what we’re seeing in stocks is driven more by hype and speculation than by real, solid fundamentals.

It’s also worth preparing ourselves for that possibility.

So, a great quarter for the markets; a not-so-great quarter for the economy. While we here at Minich MacGregor Wealth Management certainly cheer the former, we will continue watching the latter carefully. After all, that’s what you rely on us for: To keep our glasses on, and our eyes open.

In the meantime, have a great month, and a great third quarter!

1 “S&P 500, Nasdaq register best quarter since 2020 despite Iran war,” Reuters, https://www.reuters.com/business/us-stock-futures-little-changed-strong-quarter-nears-end-2026-06-30/

2 “Consumer prices rose 4.2% annually in May, highest in three years,” CNBC, https://www.cnbc.com/2026/06/10/cpi-inflation-report-may-2026.html

3 “The Index of Consumer Sentiment,” University of Michigan, https://www.sca.isr.umich.edu/files/chicsh.pdf

4 “Current and Past GDPNow Commentaries,” Federal Reserve Bank of Atlanta, https://www.atlantafed.org/research-and-data/data/gdpnow/current-and-past-gdpnow-commentaries

5 “Semiconductor stocks just had their best quarter ever,” Axios, https://www.axios.com/2026/07/01/semiconductor-ai-stocks-chips

6 “Mag 7 value shrinks by $2.3 trillion,” CNBC, https://www.cnbc.com/2026/06/30/magnificent-7-stocks-sell-off-investors-grow-jittery-on-ai-spending.html

7 “Americans’ Finances are Improving – But Some Still Feel Behind,” Northwestern Mutual, https://news.northwesternmutual.com/2026-03-09-Americans-Finances-are-Improving-But-Some-Still-Feel-Behind-and-are-Turning-to-Prediction-Markets,-Sports-Betting-and-Crypto-to-Catch-Up,-According-to-Northwestern-Mutuals-2026-Planning-Progress-Study

8 “Americans have more money in stocks than ever before. Economists say that’s a bright red flag,” CNN Business, https://www.cnn.com/2025/09/28/business/us-stocks-record-highs-american-households