Q2 2024 Market Outlook

Did you fill out a March Madness bracket this year?

If you did, or if you ever have before, you know what a challenge it can be to predict what will happen during the annual NCAA Basketball Tournament. Maybe you should just pick the higher-seeded team in every game. After all, they’re seeded higher for a reason, right? Or maybe you think a lower-ranked team will surprise everyone and beat one of the favorites. It happens every year, doesn’t it? Or maybe you’ll just look to see which teams enter the tournament on a “hot streak” and bet their winning ways will continue.

Or maybe you’ll just pick whichever mascot you like best.

Whatever strategy you use, every decision forces you to question what you think you know. Is that top-seeded team’s record for real, or does it hide the real story? If that underdog David manages to slay the heavily favored Goliath, will it continue winning, or will its story end in the next round? Does Team A’s superior shooting outweigh Team B’s better defense? The fact is that there are a million ways to guess, but there’s no single way to know.

The reason we mention all this is because many investors are facing a similar March Madness-style dilemma with the markets right now.

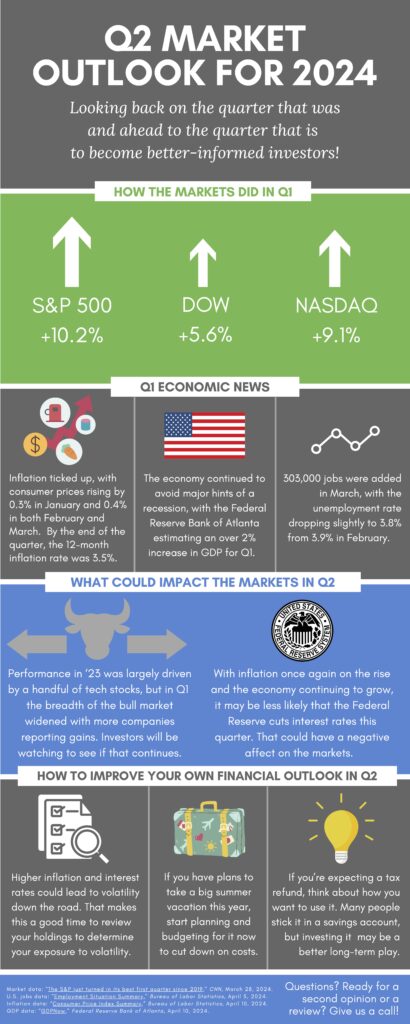

Last year, the markets surprised many experts who had predicted a recession by going on a tear. The S&P 500 finished 2023 up 24%.1 That hot streak continued through the first quarter of 2024. The S&P gained 10.2% in Q1, its best start to a year since 2019. The NASDAQ finished up 9.1%. And the Dow saw a 5.6% gain.2

This performance was largely driven by one thing: Expectation.

Now, expectation always drives the markets, more or less. Market performance is dictated by what investors expect will happen in the future based on data they’re seeing now. In a sense, every investor, expert or amateur, is filling out their own version of a March Madness bracket whenever they make a decision, but for individual companies rather than individual teams…or for the markets as a whole.

What’s less common is when such high expectations are centered around two very specific things:

Because many investors expect that one or both things will happen, they want to be positioned to take advantage of them when they do. So, more money flows into the stock market – especially into companies that would seem to benefit most from these developments – and we experience the kind of quarter that we just saw.

But now, that leaves investors with questions. Questions that are eerily like what sports fans ask themselves when filling out a bracket.

Okay, that last one isn’t real. But the rest are real questions that investors – expert and amateur – are asking themselves.

And just like with your bracket, there are a thousand ways to guess the answers. For example, here are a few arguments – all based on statistics – for why the market’s Q1 performance is “real.” (Which is to say, sustainable.)

Inflation is much lower than it was last year, and the Fed has specifically said it wants to cut rates this year. By the end of February, the Consumer Price Index was at 3.2%, whereas in February of 2023, it was at 6%.3

The economy remains strong. Corporate earnings appear healthy, the most recent unemployment rate was 3.9%4, and the Fed’s latest estimate was a 2.5% increase in GDP during Q1.5

The market’s performance is actually broadening. It’s an open secret that a major portion of the market’s gains last year were driven by just a small handful of tech companies. (Most of which are major players in the AI race.) But that portion broadened significantly in Q1. Approximately 23% of the companies in the S&P 500 reached 52-week highs.6 And if you gave each company in the S&P 500 an equal weight, the index rose 25% since October.6 (If you gave each company an equal weight in 2023, the index would have only gone up 12% for the year instead of 24%.7) In other words, more companies are driving the markets rather than just a few. And that’s good!

But there are equally compelling arguments for why the market’s performance may not be sustainable. For example:

Inflation ticked up in Q1 and the Fed has said they’re in no hurry to cut rates. Consumer prices increased by 0.4% in February after rising 0.3% in January.8 This was largely due to seasonal factors – prices usually go up in winter, partially because fuel tends to be more expensive – but it means the Fed must be even more cautious about lowering interest rates prematurely. If investors stop expecting rate cuts soon, the markets may well pull back.

Stocks may be overvalued. When you divide the size of the U.S. stock market against the size of the economy, you can see how fast the stock market is growing compared to GDP. If the ratio is heavily skewed in favor of the stock market, it suggests stocks are overvalued relative to how much the economy is producing. Right now, that ratio is near a two-year high.6

The hype around AI may be overblown. Recent technological advances have investors salivating at the possibility that AI will help companies produce more at lower cost…and by doing so, return more value to their shareholders. But this hype has been going on for well over a year now. How much AI has contributed in terms of tangible results is an open question. Developing AI technology is extremely expensive, so if investors decide the return is not worth the expense, the hype may die out.

So, like with a March Madness bracket, how do we decide what to predict? Which argument, which statistics, matter?

The answer: All of them…and none of them.

Here at Minich MacGregor Wealth Management, we pay attention to all these statistics but are beholden to none. We use statistics to be alert to any possible opportunities and to be wary of any potential pitfalls. In other words, we use statistics to help us be prepared for possibilities…not to make predictions.

You see, what really matters is that we don’t treat investing like March Madness.

When you fill out a bracket, you are then locked into whatever choices you made. If you make a wrong choice, you must live with it. It’s too late to change anything. But our strategy is far more flexible. Imagine you filled out a bracket but could then adjust in real time depending on how different games were trending. Furthermore, imagine you could exit out of your bracket altogether, if necessary, and then start participating again later.

That’s what we can do every day with the markets. Furthermore, we’re able to focus on the metrics that are proven to matter: Primarily, the law of supply and demand. As a result, we don’t have to make predictions, hope we’re right, and then hold on no matter what. We measure how various stocks and sectors – or teams and regions, in March Madness parlance – are trending. When they trend above a certain point, we play offense with your portfolio. When they trend below, we play defense. Experience has convinced us that this approach – being flexible and adaptable – is the surest way to your destination.

As always, though, let us know if you have any questions or concerns. While we’re hardly qualified to give bracket advice, our team is always here to help you with a different sort of Big Dance: The one that takes place where you want it, when you want it, with the people you want to share it with.

1 “Stocks close out 2023 with a 24% gain,” CBS, www.cbsnews.com/news/stock-market-up-24-percent-2023-rally/

2 “The SP 500 just turned in its best first quarter since 2019,” CNN Business, www.cnn.com/2024/03/28/investing/premarket-stocks-trading-first-quarter/index.html

3 “12-month percentage change, CPI,” U.S. Bureau of Labor Statistics, www.bls.gov/charts/consumer-price-index/consumer-price-index-by-category-line-chart.htm

4 “The Employment Situation – February 2024,” U.S. Bureau of Labor Statistics, www.bls.gov/news.release/pdf/empsit.pdf

5 “GDPNow,” Federal Reserve Bank of Atlanta, www.atlantafed.org/cqer/research/gdpnow

6 “Warren Buffett’s favorite market indicator is flashing red,” CNN Business, www.cnn.com/2024/03/27/investing/premarket-stocks-trading/index.html

7 “S&P 500 Equal Weight Index” https://www.spglobal.com/spdji/en/indices/equity/sp-500-equal-weight-index/#overview

8 “Consumer Price Index – February 2024,” U.S. Bureau of Labor Statistics, www.bls.gov/news.release/cpi.nr0.htm